Ethanol Margins March 30, 2026

March marks the end of the seasonal slowdown for ethanol. Maintenance outages are underway, with most plants taking 5–7 days offline ahead of summer, tightening supply after February stock builds.<stocks>

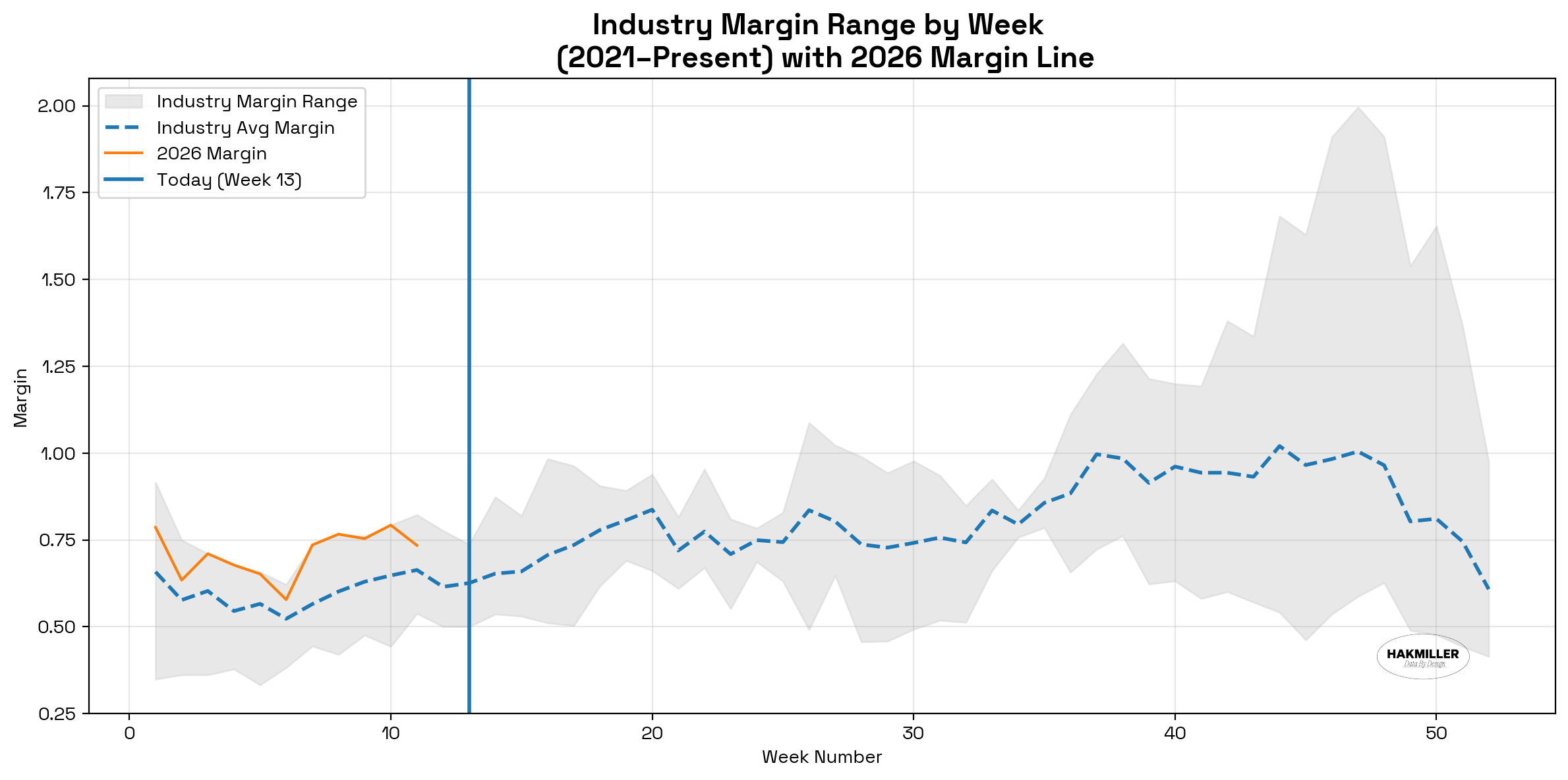

Corn is supportive this year, though not evenly—Northwest plants continue to outperform the Southeast. Corn remains the largest cost input, and regional pricing is driving margin differences. CBOT corn is ~$0.30 below last year, while ethanol prices are ~$0.10 higher, supporting margins. <basis>

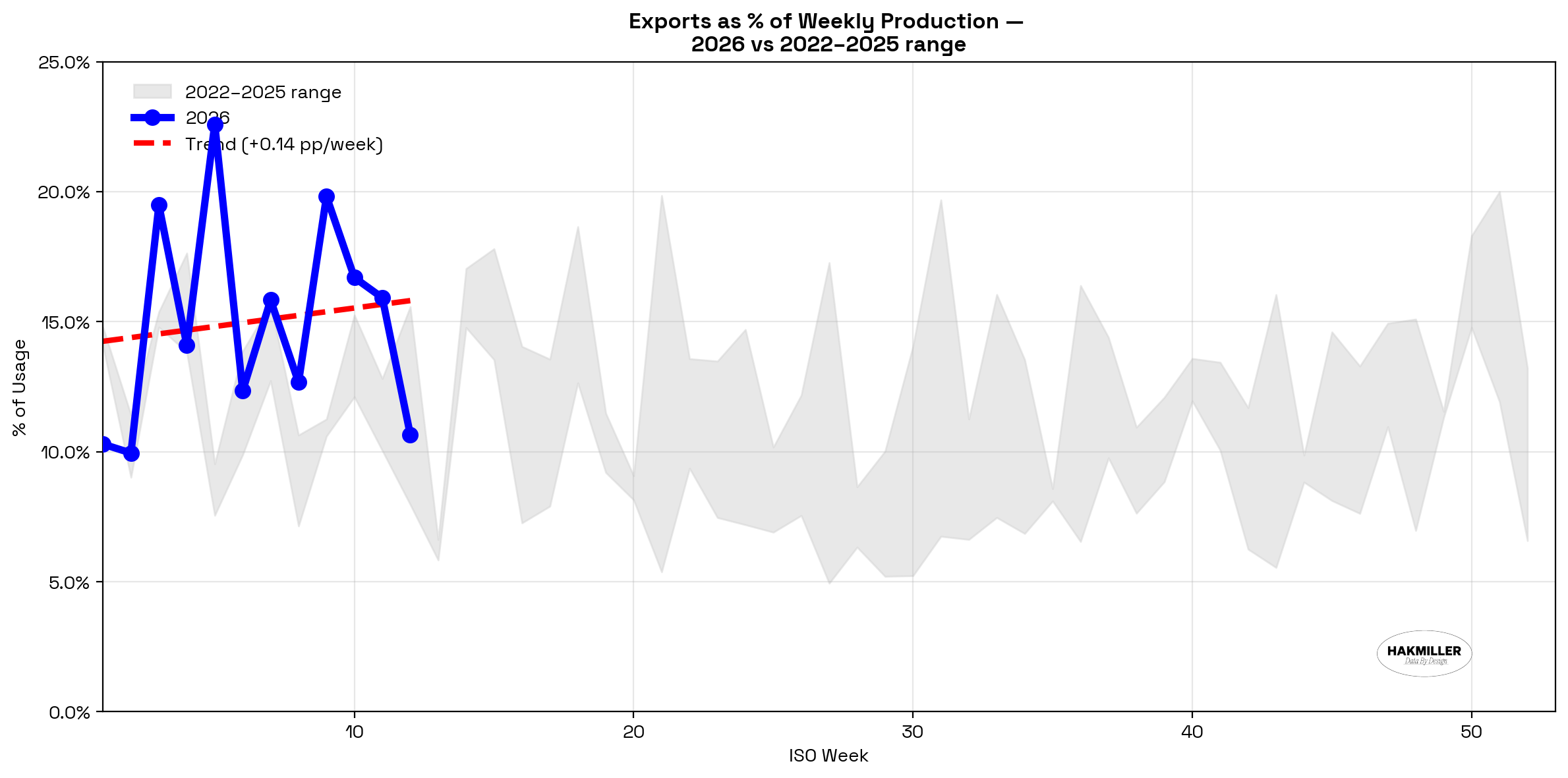

The combination of lower feedstock costs and stronger ethanol pricing is producing above-normal margins for this time of year. Export demand remains strong, keeping stocks at the low end of historical ranges heading into peak demand season. <exports>

{kind=link}

With stocks already tight, they are likely to remain constrained through Labor Day. Alongside supportive RVO levels and continued momentum toward year-round E15, the outlook points to sustained profitability—making ethanol a relative bright spot in the ag sector. <margin>

{kind=link}